All Categories

Featured

Table of Contents

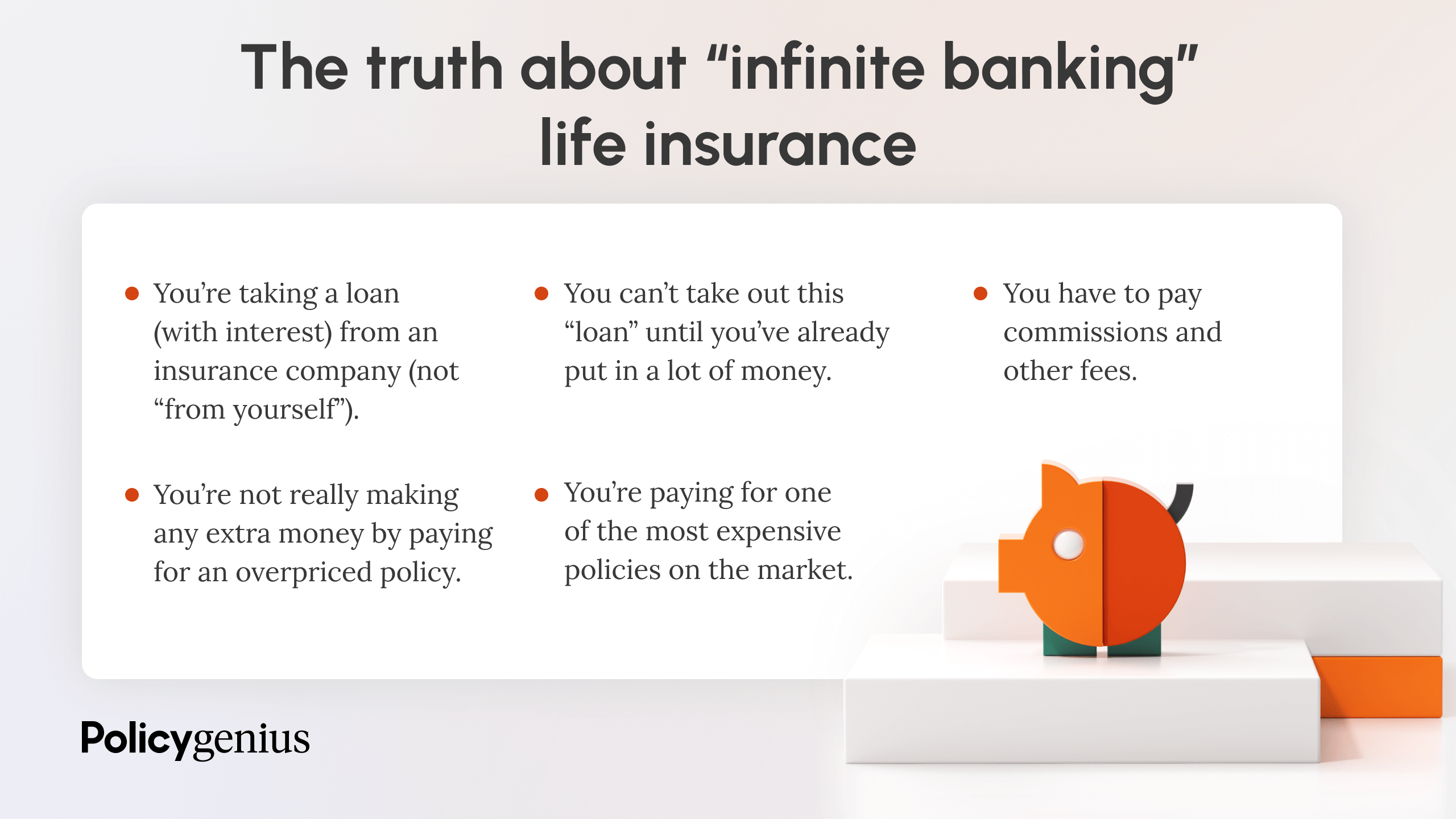

The are entire life insurance and global life insurance coverage. The money value is not added to the fatality benefit.

The policy lending interest price is 6%. Going this route, the rate of interest he pays goes back into his plan's money value rather of a financial establishment.

Think of never needing to fret about small business loan or high rates of interest once more. Suppose you could obtain money on your terms and develop wide range at the same time? That's the power of unlimited banking life insurance. By leveraging the cash value of entire life insurance IUL policies, you can grow your riches and obtain cash without depending on standard financial institutions.

There's no collection car loan term, and you have the liberty to choose on the repayment timetable, which can be as leisurely as paying off the financing at the time of fatality. This flexibility reaches the servicing of the finances, where you can choose for interest-only settlements, maintaining the lending balance flat and workable.

Holding cash in an IUL fixed account being attributed rate of interest can often be far better than holding the money on down payment at a bank.: You've constantly imagined opening your very own bakeshop. You can obtain from your IUL policy to cover the preliminary expenditures of renting out a space, buying devices, and working with team.

Bioshock Infinite Bank Of Columbia

Personal car loans can be gotten from standard financial institutions and cooperative credit union. Below are some bottom lines to think about. Credit rating cards can supply a flexible means to borrow money for very short-term periods. Obtaining money on a debt card is typically really expensive with yearly percentage prices of rate of interest (APR) commonly reaching 20% to 30% or more a year.

The tax treatment of policy fundings can vary significantly depending upon your nation of home and the details terms of your IUL plan. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, policy financings are typically tax-free, using a substantial advantage. Nonetheless, in other territories, there may be tax ramifications to think about, such as possible tax obligations on the finance.

Term life insurance policy only supplies a fatality advantage, without any type of money value accumulation. This suggests there's no cash money value to borrow versus. This post is authored by Carlton Crabbe, Ceo of Funding forever, a professional in providing indexed global life insurance policy accounts. The details supplied in this write-up is for instructional and educational purposes only and need to not be taken as financial or investment recommendations.

Infinite Banking Forum

When you first read about the Infinite Financial Concept (IBC), your initial response may be: This appears as well excellent to be true. Perhaps you're hesitant and think Infinite Banking is a rip-off or system - infinite bank statements. We want to set the document directly! The problem with the Infinite Banking Idea is not the concept however those individuals providing an unfavorable critique of Infinite Financial as an idea.

As IBC Authorized Practitioners through the Nelson Nash Institute, we assumed we would certainly address some of the top inquiries individuals search for online when discovering and understanding everything to do with the Infinite Banking Principle. What is Infinite Banking? Infinite Banking was created by Nelson Nash in 2000 and fully described with the publication of his publication Becoming Your Own Lender: Open the Infinite Financial Concept.

Infinite Banking Example

You think you are coming out economically ahead due to the fact that you pay no rate of interest, however you are not. With saving and paying cash money, you may not pay passion, however you are utilizing your cash as soon as; when you spend it, it's gone for life, and you offer up on the opportunity to make life time substance interest on that money.

Billionaires such as Walt Disney, the Rockefeller family and Jim Pattison have actually leveraged the residential properties of entire life insurance policy that dates back 174 years. Also financial institutions utilize entire life insurance policy for the same functions. It is called Bank-Owned-Life-Insurance (BOLI). The Canada Revenue Agency (CRA) even acknowledges the worth of taking part whole life insurance policy as an one-of-a-kind asset class used to generate long-term equity securely and predictably and provide tax obligation benefits outside the range of standard financial investments.

How To Start Infinite Banking

It enables you to create wide range by satisfying the financial feature in your very own life and the capability to self-finance major way of life purchases and expenditures without disrupting the compound passion. Among the most convenient ways to consider an IBC-type participating entire life insurance policy plan is it approaches paying a home loan on a home.

When you obtain from your getting involved whole life insurance coverage plan, the cash value continues to expand continuous as if you never ever obtained from it in the initial place. This is because you are utilizing the money worth and fatality benefit as collateral for a financing from the life insurance coverage company or as collateral from a third-party lender (recognized as collateral lending).

That's why it's critical to deal with a Licensed Life insurance policy Broker authorized in Infinite Banking who frameworks your participating entire life insurance coverage policy properly so you can prevent adverse tax obligation implications. Infinite Banking as a financial technique is except every person. Here are some of the benefits and drawbacks of Infinite Banking you need to seriously take into consideration in determining whether to progress.

Our recommended insurance policy provider, Equitable Life of Canada, a shared life insurance coverage company, focuses on participating whole life insurance policy policies certain to Infinite Banking. Additionally, in a common life insurance policy firm, insurance holders are thought about business co-owners and get a share of the divisible excess created every year through rewards. We have a selection of providers to pick from, such as Canada Life, Manulife and Sunlight Lifedepending on the demands of our clients.

Please additionally download our 5 Top Questions to Ask An Infinite Banking Representative Prior To You Work with Them. To learn more concerning Infinite Financial go to: Disclaimer: The product provided in this newsletter is for educational and/or academic functions only. The details, opinions and/or sights shared in this e-newsletter are those of the authors and not always those of the representative.

Ibc Infinite Banking Concept

The idea of Infinite Financial was created by Nelson Nash in the 1980s. Nash was a financing professional and follower of the Austrian college of business economics, which supports that the worth of goods aren't explicitly the result of traditional financial structures like supply and demand. Rather, people value cash and items in different ways based on their financial status and requirements.

One of the pitfalls of typical banking, according to Nash, was high-interest rates on loans. Too numerous individuals, himself consisted of, got into monetary difficulty due to dependence on banking institutions.

Infinite Financial needs you to have your economic future. For goal-oriented individuals, it can be the ideal financial device ever before. Here are the advantages of Infinite Financial: Arguably the solitary most helpful facet of Infinite Financial is that it boosts your cash flow.

Dividend-paying entire life insurance is very reduced threat and offers you, the insurance policy holder, a fantastic offer of control. The control that Infinite Financial offers can best be organized into two groups: tax advantages and asset protections. One of the reasons entire life insurance is optimal for Infinite Banking is how it's strained.

Entire life insurance coverage policies are non-correlated assets. This is why they work so well as the economic foundation of Infinite Financial. Regardless of what happens in the market (supply, real estate, or otherwise), your insurance coverage plan retains its well worth.

Entire life insurance is that 3rd pail. Not only is the price of return on your entire life insurance policy assured, your fatality advantage and costs are also guaranteed.

Infinite Banking Concept Dave Ramsey

Infinite Banking allures to those looking for higher monetary control. Tax obligation performance: The cash money value grows tax-deferred, and plan finances are tax-free, making it a tax-efficient device for developing wide range.

Asset defense: In many states, the cash worth of life insurance policy is secured from financial institutions, adding an extra layer of financial safety and security. While Infinite Banking has its qualities, it isn't a one-size-fits-all solution, and it features substantial drawbacks. Below's why it might not be the very best approach: Infinite Banking typically calls for intricate plan structuring, which can confuse policyholders.

{kind=link}

Latest Posts

Infinite Banking Concept Explained

Be Your Own Bank

Start Your Own Personal Bank